The Medicare Decision You Can't Take Back

Most people planning to retire abroad spend months researching cost of living, visa options, and which neighborhoods feel right. They build spreadsheets. They watch videos. They join Facebook groups and ask questions at midnight.

And then they leave, without ever making a deliberate decision about Medicare Part B.

That’s not a small oversight. It’s a permanent one.

I’m Mike , and along with MJ, we’re the global nomads behind The GenXit Project. We’ve spent a lot of time in the weeds on this particular topic. What we found is that the Medicare question isn’t really about healthcare. It’s about a door that, once closed, costs you real money to reopen, and the longer it stays closed, the more expensive that gets.

👉 Watch the full episode: What Happens to Your Social Security and Medicare When You Retire Abroad

Your Social Security Isn’t Going Anywhere

Before we get into the hard stuff, here’s the piece of this that actually works in your favor.

Your Social Security benefits follow you. If you’re a US citizen who earned those credits, you can move to Colombia, Thailand, Panama, Portugal, Mexico, pretty much anywhere you’d realistically want to live, and your monthly payment keeps arriving. No reduction. No pause. No penalty for leaving.

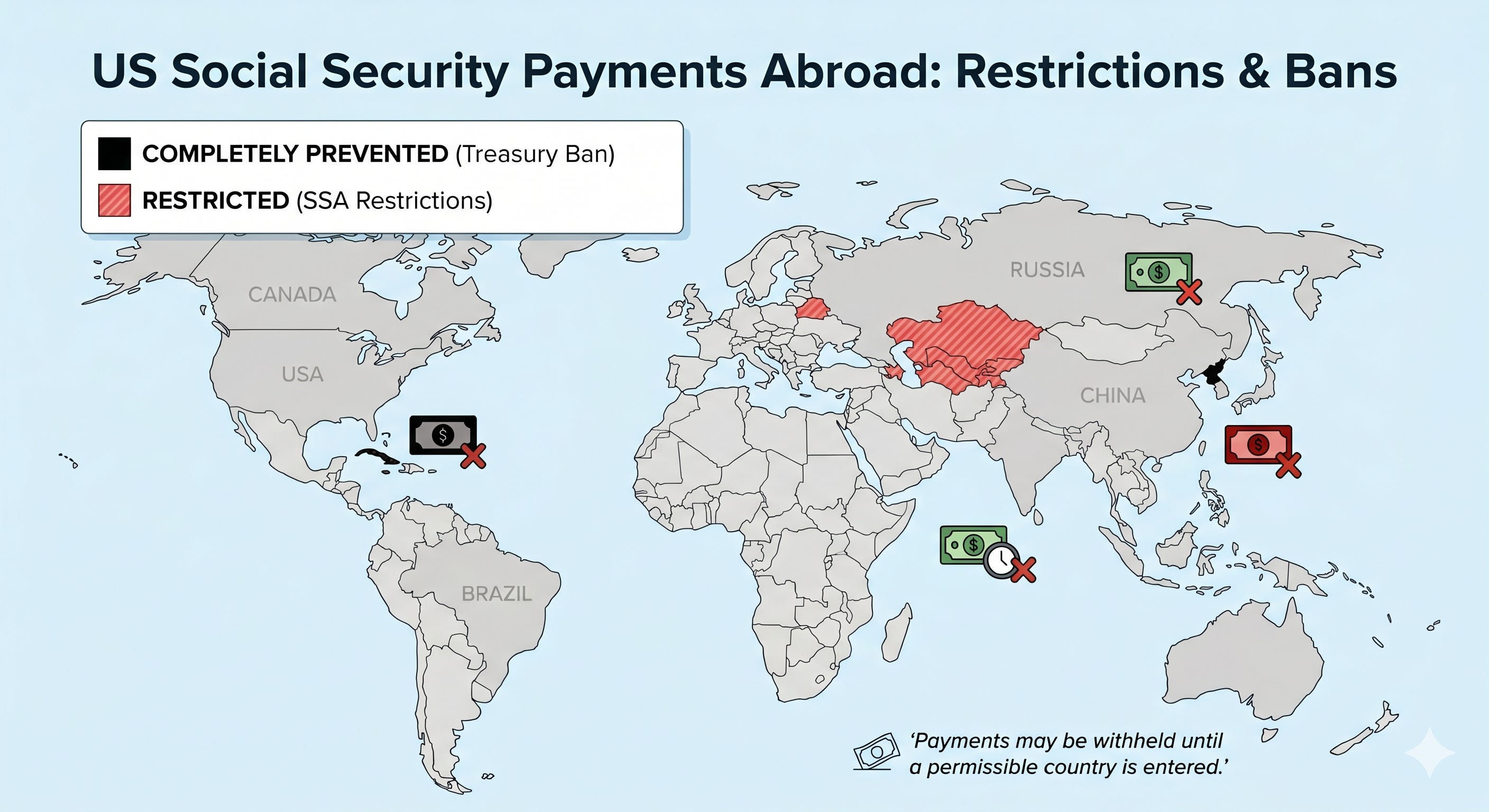

The map of places where the US can’t send your money is genuinely short. Cuba and North Korea are the hard blocks. A small cluster of former Soviet republics carries some restrictions. That’s essentially it.

What does trip people up is something far more mundane. Social Security sends a questionnaire every one to two years to confirm you’re still alive and still eligible. Miss it, or miss it because it went to an old address you no longer check, and they stop your payments.

Before you leave the US, set up your online account at ssa.gov and keep your address current. When that form shows up, treat it like the bill that keeps your lights on. Because it is.

We covered the full details of collecting Social Security abroad — including how to use the SSA's own screening tool to check your specific country in about two minutes — in a separate article. Read: Can You Really Get Your Social Security Check While Living Abroad?

“Social Security Won’t Even Exist By the Time You Retire”

We’ve all heard some version of that sentence our entire adult lives.

When I was 25 and newly licensed as a financial advisor, I sat across from clients in their 50s who said exactly that. This was the 1990s. The fear was everywhere. And those same clients eventually retired, collected their benefits, and a good number of them are still collecting today.

Now MJ and I are in our 50s, and the fear is back, louder than ever, with more reasons to feel real. We get it. Nothing about the current environment makes long-term planning feel simple.

Here’s how I approach it. I can’t build a retirement plan around something that hasn’t happened. What I can do is plan carefully for the rules as they exist today, stay informed, and stay flexible. Abandoning a well-researched plan because of a fear that’s been predicting the same outcome since the Reagan administration is probably not your best move.

Plan for what you know. Adapt if things change.

The Non-Citizen Spouse Detail Nobody Talks About

If your partner isn’t a US citizen, your destination choice carries more weight than you might realize.

A non-citizen spouse who moves outside the US can lose access to survivor benefits after just six months abroad. That’s a real exposure, and one that’s surprisingly easy to avoid if you know to look for it.

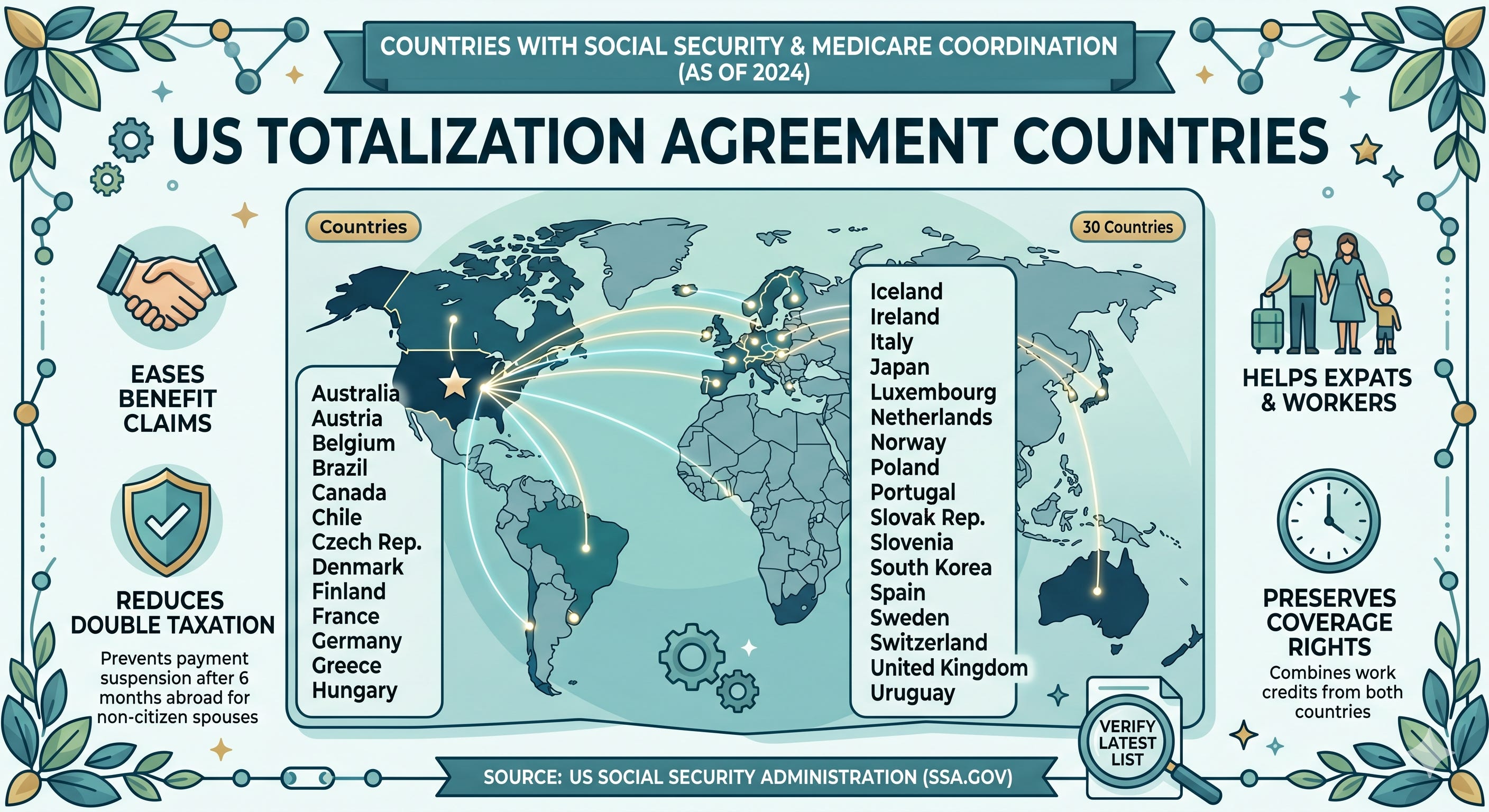

The US has Totalization Agreements with about 30 countries. These agreements are mainly designed to prevent double taxation on Social Security, but they come with a significant side benefit: they protect non-citizen spouses from that six-month cutoff. If your destination is on the list, you’re in a much friendlier situation.

Spain, Portugal, France, Italy, Germany, Japan, Australia, and the UK are all on the list. Colombia, Thailand, Panama, Mexico, and the Philippines are not.

That doesn’t mean those countries are off the table. It means the non-citizen spouse situation requires a separate conversation with someone who knows the specifics of your country and your circumstances. This is a before-you-go detail, not an after-you-land detail.

Now for the Part That Actually Keeps People Up at Night

Your Social Security travels with you. Your Medicare does not.

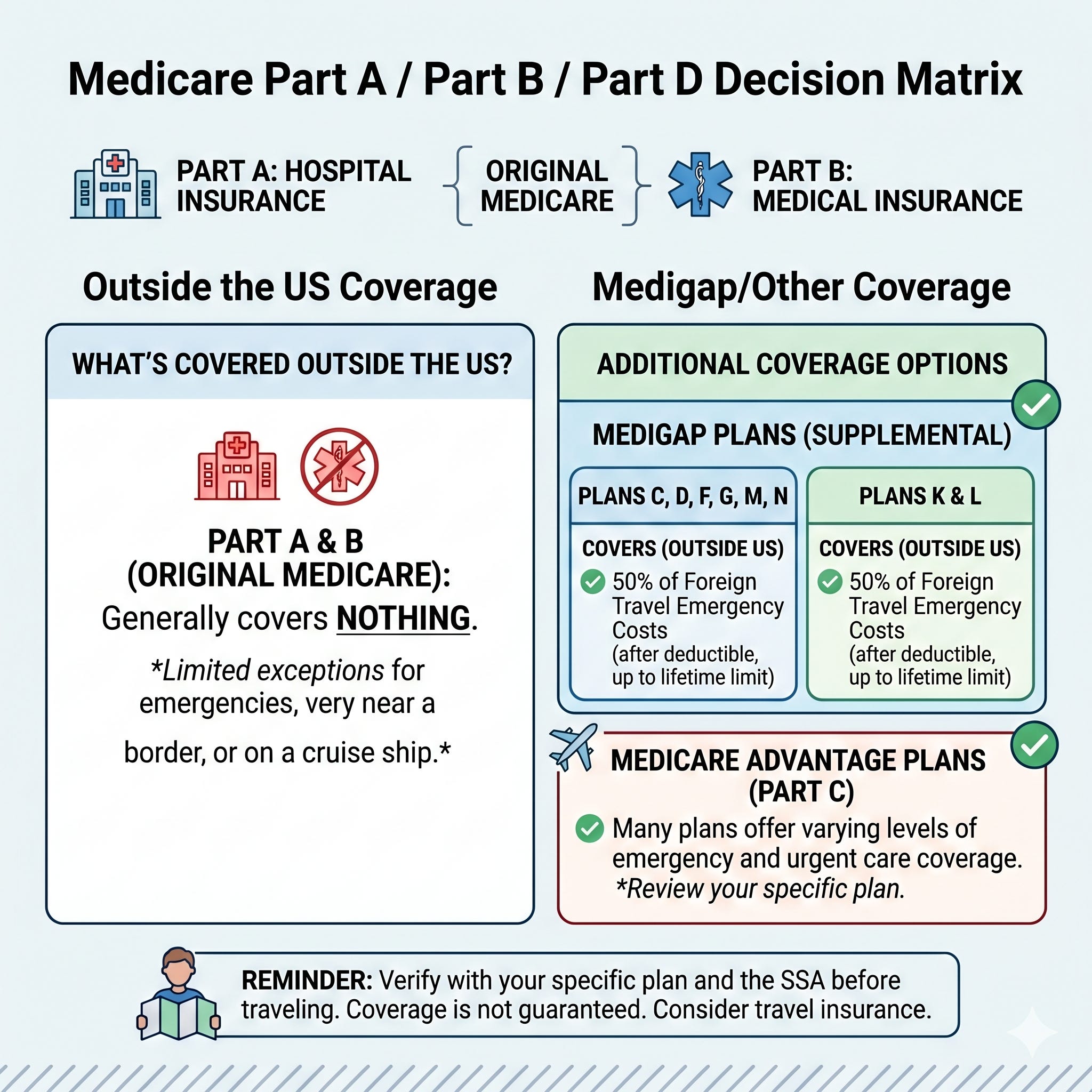

Original Medicare, Part A and Part B, covers essentially nothing outside the United States. You can be enrolled. You can be paying. And the moment you’re living in another country, that coverage is nearly useless for your day-to-day life there.

The natural reaction is to cancel it and redirect that money toward something that actually works where you live. That reaction is understandable. It also walks you straight into a permanent cost.

Part A: The Easy Call

Part A is hospital coverage, and for most people it’s premium-free. You paid for it through decades of payroll taxes. Since it costs you nothing to keep, keep it. This one’s simple.

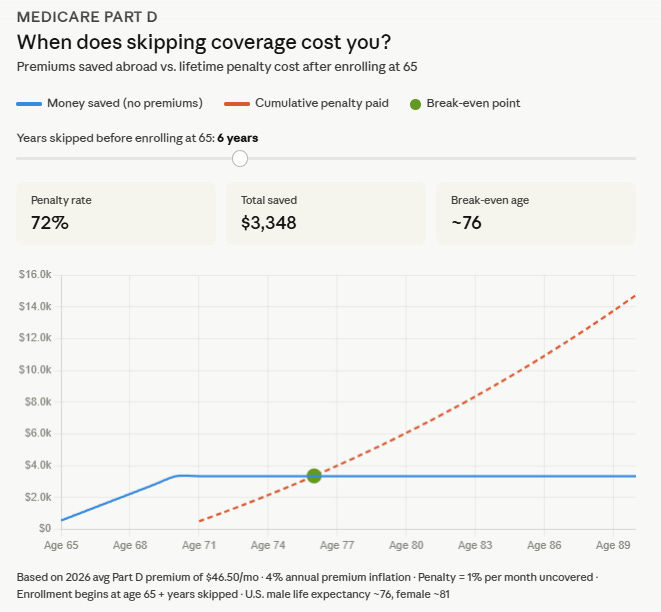

Part B: The Decision That Follows You Forever

Part B is where things get real. This is your doctor and outpatient coverage, and it runs around $202.90 a month in 2026 depending on your income.

If Medicare doesn’t work where you’re living, it’s tempting to drop it and save that money. Some people do exactly that, and for some people, it works out fine.

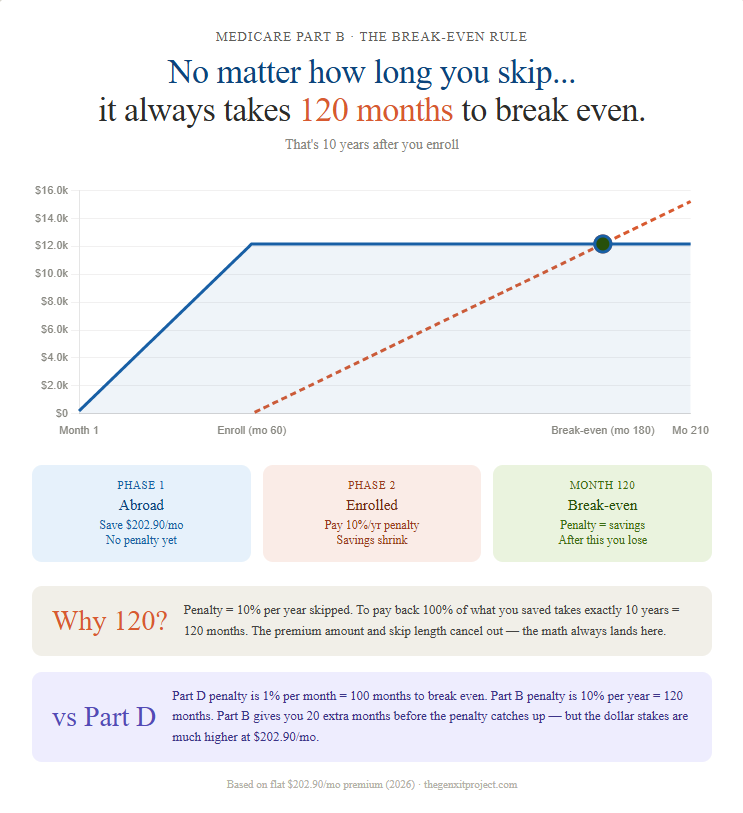

But Part B has a late enrollment penalty built into it. If you drop it and later want it back, you pay an additional 10% on your premium for every 12-month period you went without coverage. That penalty is permanent. It doesn’t age off. It lives on your premium for as long as you have Part B.

The math reality: no matter how many years you skip, it always takes exactly 120 months, ten years, after you re-enroll for the penalty costs to exceed what you saved. That’s the break-even point.

So skipping Part B while you’re abroad isn’t automatically a bad financial decision. But it is a one-way door. Once you drop it, the clock starts.

The real question isn’t whether Part B is useful abroad. It isn’t. The real question is whether you ever see yourself flying back to the US for a major procedure, a serious diagnosis, or a planned surgery. Medicare doesn’t care where you live, it cares where you are. If you keep Part B active, you can land at O’Hare and have full coverage the moment you clear customs.

Think of it like paying storage on something valuable. You’re not using it daily. But if you ever need it, you’ll be glad it’s there.

One important nuance here: if flying home for care is part of your backup plan, Original Medicare is what makes that work cleanly. Medicare Advantage plans are built around local networks. Step outside your service area and you have real gaps. Advantage plans offer some emergency coverage abroad, but they’re designed for travelers and snowbirds, people on a trip, not people who live there. Read that fine print before you rely on it.

What About Medigap?

This is something worth knowing before you make the Part B decision.

Certain Medigap supplemental plans, specifically Plans C, D, F, G, M, and N, cover 50% of foreign travel emergency costs, after a deductible and up to a lifetime limit. That’s not nothing. If a true emergency happens and you’re not on home turf, having a Medigap plan active alongside Part B gives you a layer of protection that standard Medicare alone doesn’t.

It’s not a substitute for local coverage or a real international health policy. But it’s a piece of the picture worth knowing about when you’re deciding whether to keep Part B active during your years abroad.

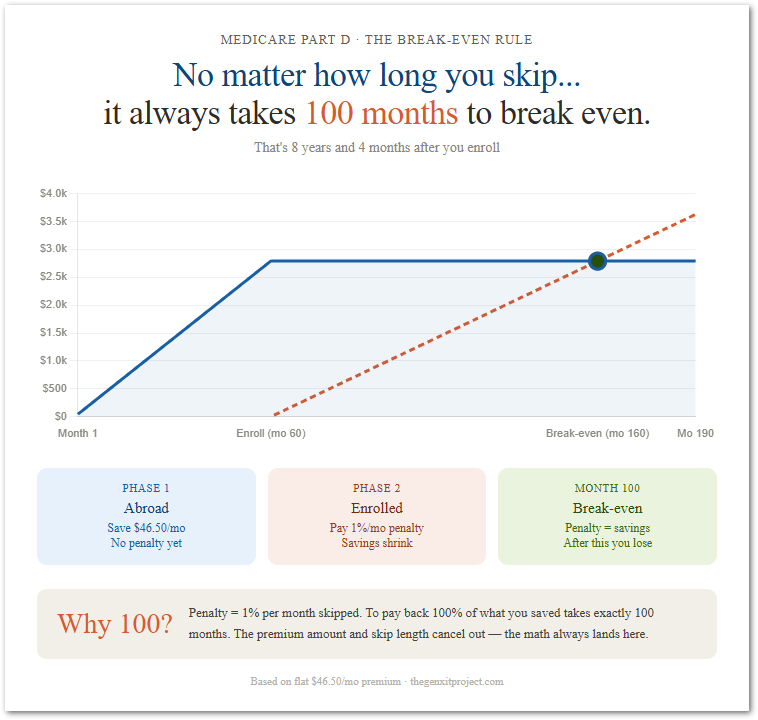

Part D: Skip It, But Know the Price

Part D covers prescription drugs, and it doesn’t work overseas. There’s no real argument for paying those premiums while you’re living abroad.

When you eventually return to the US permanently, you get a two-month window to enroll. The catch is that those years abroad almost certainly won’t qualify as creditable coverage under Medicare’s standards, so you’ll carry a late enrollment penalty based on how long you were gone.

The good news is that the math is more manageable than it sounds. No matter how many years you skip Part D, the break-even point after you re-enroll is always 100 months, 8 years and 4 months. Skip 6 years abroad, pay the penalty when you return, and you’d still need to be back in the US and enrolled for over 8 years before the penalty costs exceed what you saved.

That’s a real cost. It’s worth knowing about. It’s not a reason to cancel your plans.

A Note on These Numbers

The break-even figures shown here use flat premiums for clarity. We didn’t factor in annual premium inflation, and we also didn’t credit the savings you’d earn if you invested those premiums during your years abroad instead of paying them. Those two forces roughly offset each other, but reasonable people can model it differently. The simple numbers give you a clean baseline to work from.

There’s also a life expectancy angle worth considering. If the break-even point after re-enrolling is 100 months and your realistic life expectancy at that age is shorter than that, the penalty math may actually work in your favor. That’s a personal calculation, but it’s a real one.

None of this is financial advice, and I am not your financial advisor. These numbers are here to help you ask better questions, not to make the decision for you. Before you do anything with your Medicare coverage, talk to a professional who knows your full picture.

What Actually Covers You Where You Live

So if Medicare is essentially parked while you’re abroad, what replaces it?

The setup most global nomads end up running is two layers. First, local health coverage in your destination country, this handles routine visits, prescriptions, and the unexpected. In most of the destinations we research, this is dramatically more affordable than what we’re used to paying in the US. Real doctors, real hospitals, real coverage.

Second layer is an international health insurance policy for the bigger scenarios, serious illness, medical evacuation, the kind of coverage that works regardless of which country you’re standing in when something goes wrong.

There’s a third path some global nomads take that sounds reckless to American ears but makes more sense once you’ve seen what healthcare actually costs in most target destinations: paying out of pocket entirely, with no insurance at all.

That sentence probably made your stomach drop.

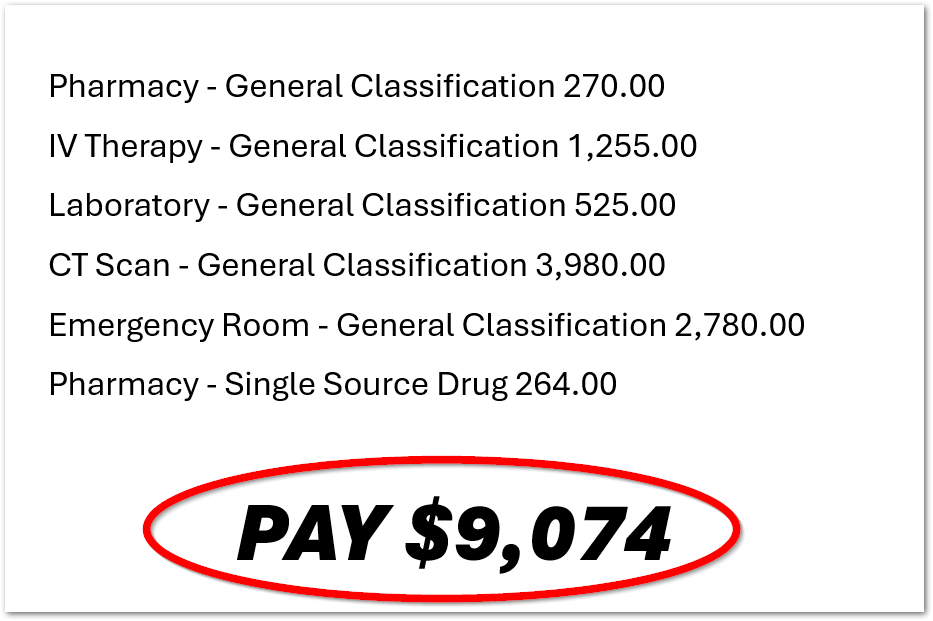

That reaction makes complete sense if your entire frame of reference is the US healthcare system. I recently got a bill for an emergency room visit, a kidney stone, a few hours in the ER, nothing requiring surgery or admission. The bill came in at over $9,000. My insurance covered most of it, but my out-of-pocket hit was still $1,200.

For a kidney stone.

In a lot of the countries we research, Thailand, Mexico, Colombia, the Philippines, that same visit might run $200 to $500 cash, no insurance involved. A specialist consultation that costs $400 in Chicago might be $25 in Chiang Mai. The math on self-pay looks completely different when the underlying prices are completely different.

We’re not recommending you go without coverage. Catastrophic care, serious surgeries, cancer treatment, medical evacuation, is where the real financial exposure lives, and that’s exactly what an international policy is designed for. But understanding that the baseline cost of care is fundamentally different abroad is important context for how global nomads actually think about this decision.

One thing worth knowing early: many international health plans have age caps on new enrollees. Some won’t accept new members past 65 or 70. If you’re waiting until after you’ve retired to sort this out, some of those doors may already be closing. This is research-before-you-leave territory, not figure-it-out-when-you-land territory.

We’ll be covering specific insurance options as we dig into individual destinations. For now, the frame that matters is: plan as if Medicare doesn’t exist where you’re going. Because for practical purposes, it doesn’t.

One More Practical Note: How to Receive Your Money

The consensus from people already living this life is consistent on this one. Keep your Social Security depositing into a US bank account. Don’t route it directly to a foreign bank. US banking is stable, familiar, and clean from a paperwork standpoint.

Then transfer what you need locally using a service like Wise, which offers competitive exchange rates and much lower fees than traditional international wire transfers.

Simple setup. Reliable. Easy to manage from anywhere in the world.

The Bottom Line

Your income travels with you. Your Medicare mostly doesn’t. The decisions you make about Part B, specifically, whether to keep it or drop it before you leave, follow you permanently.

If you’re still two or three years out from your exit date, that’s actually good news. You have time to make these decisions deliberately instead of reactively. You have time to talk to the right professionals, research your destination’s healthcare options, and sort out your international coverage before the age caps on some policies quietly close.

Every one of these traps is avoidable. But only if you handle it before you go.

Not sure how your savings and timeline translate into an actual exit date? That’s exactly what our Bridge Fund Calculator is designed to show you, a practical way to visualize the gap between today and your freedom date.

👉 Link to Bridge Fund Calculator here

Links Mentioned in This Article

Set up your Social Security account: ssa.gov

Transfer money internationally: Wise

Watch: Which Countries Are Friendly for Social Security Recipients

Watch the full episode: What Happens to Your Social Security and Medicare When You Retire Abroad

Who We Are

Mike and MJ are the voices behind The GenXit Project, a resource for Gen X professionals exploring early retirement, financial independence, and life abroad. We cover international relocation, expat finance, and the real logistics of leaving it all behind, in the best way. Follow our journey on YouTube and the website as we turn “what if” into “what’s next.”